The life of a business is divided into accounting periods, which is the time frame (usually a fiscal year) for which a business chooses to prepare its financial statements. Unearned revenues are also recorded because these consist of income received from customers, but no goods or services have been provided to them. In this sense, the company owes the customers a good or service and must record the liability in the current period until the goods or services are provided. Since the Accumulated Depreciation account was credited in the adjusting entry rather than the Equipment account directly, the Equipment account balance remains at $6,000, its cost. The adjusting entry above is made at the end of each month for 60 months. A fixed asset is a tangible/physical item owned by a business that is relatively expensive and has a permanent or long life—more than one year.

Unearned Revenues

One of the main financial statements (along with the balance sheet, the statement of cash flows, and the statement of stockholders’ equity). The income statement is also referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement.

Mistake: Incorrect Accounting Entries

A business license is a right to do business in a particular jurisdiction and is considered a tax. During the month you will use some of this rent, but you will wait until the end of the month to account for what has expired. During the month you will use some of this insurance, but you will wait until the end of the month to account for what has expired.

Business License Tax – Deferred Expense

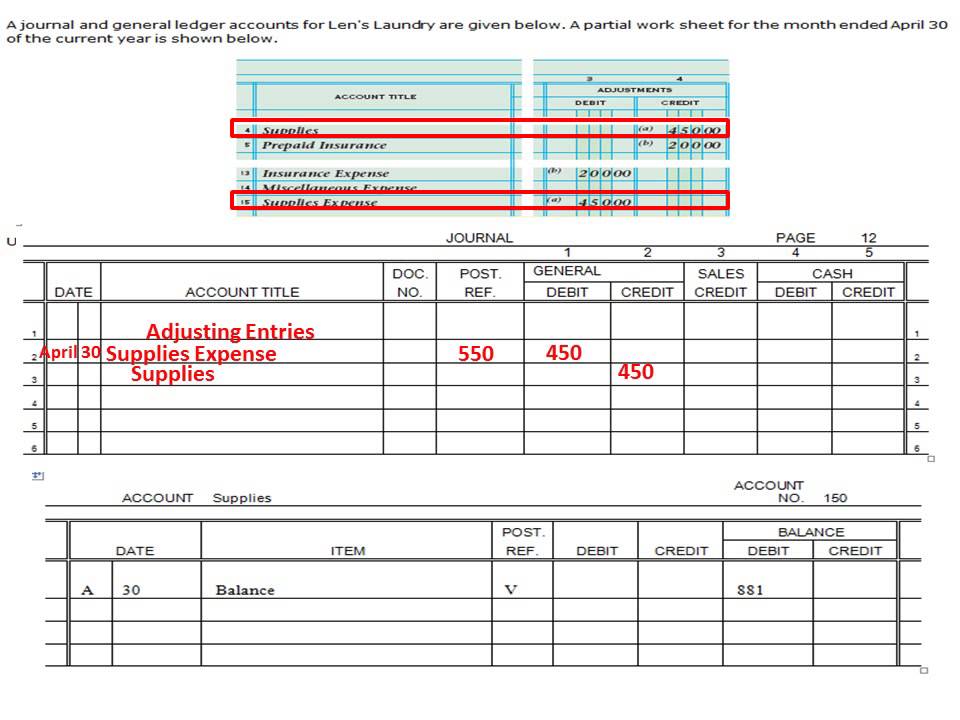

There are two changes that will be made so that the journal entry is CORRECT for depreciation. Here are the ledgers that relate to the purchase of prepaid taxes when the transaction above is posted. Here are the Supplies and Supplies Expense ledgers AFTER the adjusting entry has been expensify + xero posted. All adjusting entries include at least a nominal account and a real account. A real account has a balance that is measured cumulatively, rather than from period to period. Expenses should be recognized in the period when the revenues generated by such expenses are recognized.

Your Financial Statements At The End Of The Accounting Period May Be Inaccurate

- During the month you will use some of this rent, but you will wait until the end of the month to account for what has expired.

- To record accrued revenue, an adjusting entry is made to increase the revenue account and increase the corresponding asset account.

- The balance sheet reports the assets, liabilities, and owner’s (stockholders’) equity at a specific point in time, such as December 31.

- Such expenses are recorded by making an adjusting entry at the end of the accounting period.

Adjustment entries are not necessary under the cash basis of accounting, as all transactions are recorded when payment is made or received. To record an unearned revenue, an accountant would debit a liability account and credit a revenue account. Depreciation expense is the allocation of the cost of a long-term asset over its useful life. To record depreciation expense, an accountant would debit an expense account and credit an accumulated depreciation account.

Then, when you get paid in March, you move the money from accrued receivables to cash. Other methods that non-cash expenses can be adjusted through include amortization, depletion, stock-based compensation, etc. The adjusting entry in this case is made to convert the receivable into revenue. Now that all of Paul’s AJEs are made in his accounting system, he can record them on the accounting worksheet and prepare an adjusted trial balance. In all the examples in this article, we shall assume that the adjusting entries are made at the end of each month.

An adjusting journal entry is typically made just prior to issuing a company’s financial statements. The entry records any unrecognized income or expenses for the accounting period, such as when a transaction starts in one accounting period and ends in a later period. Since the firm is set to release its year-end financial statements in January, an adjusting entry is needed to reflect the accrued interest expense for December. The adjusting entry will debit interest expense and credit interest payable for the amount of interest from Dec. 1 to Dec. 31.

Prepaid insurance is insurance that has been paid for but not yet used. To record prepaid insurance, an adjusting entry is made to decrease the asset account and increase the corresponding expense account. Deferred revenue is revenue that has been received but not yet earned. To record deferred revenue, an adjusting entry is made to decrease the liability account and increase the corresponding revenue account.

A current asset which indicates the cost of the insurance contract (premiums) that have been paid in advance. It represents the amount that has been paid but has not yet expired as of the balance sheet date. Therefore, it is considered essential that only those items of expenses, losses, incomes, and gains should be included in the Trading and Profit and Loss Account relating to the current accounting period.

If the company would like to continue to occupy the rental property, it will have to prepay again. Here is the Insurance Expense ledger where transaction above is posted. Here is the Supplies Expense ledger where transaction above is posted. By making these adjustments, companies can ensure that their financial statements are accurate and reliable, which is important for making business decisions and meeting regulatory requirements. Adjustment entries can also impact a business’s stock-based compensation expenses.