Accumulated depreciation refers to the accumulated depreciation of a company’s asset over the life of the company. On a company’s balance sheet, accumulated depreciation is called a contra-asset account and it is used to track depreciation expenses. Adjusting entries are made at the end of an accounting period after a trial balance is prepared to adjust the revenues and expenses for the period in which they occurred.

( . Adjusting entries that convert liabilities to revenue:

After 12 full months, at the end of May in the year after the business license was initially purchased, all of the prepaid taxes will have expired. If the company would like to continue to do business voucher ideas examples 2023 in the upcoming year, it will have to prepay again. After 12 full months, at the end of May in the year after the rent was initially purchased, all of the prepaid rent will have expired.

- The adjusting entry in this case is made to convert the receivable into revenue.

- This reduction is essential for presenting a realistic value of the company’s assets, which in turn affects the equity section of the balance sheet.

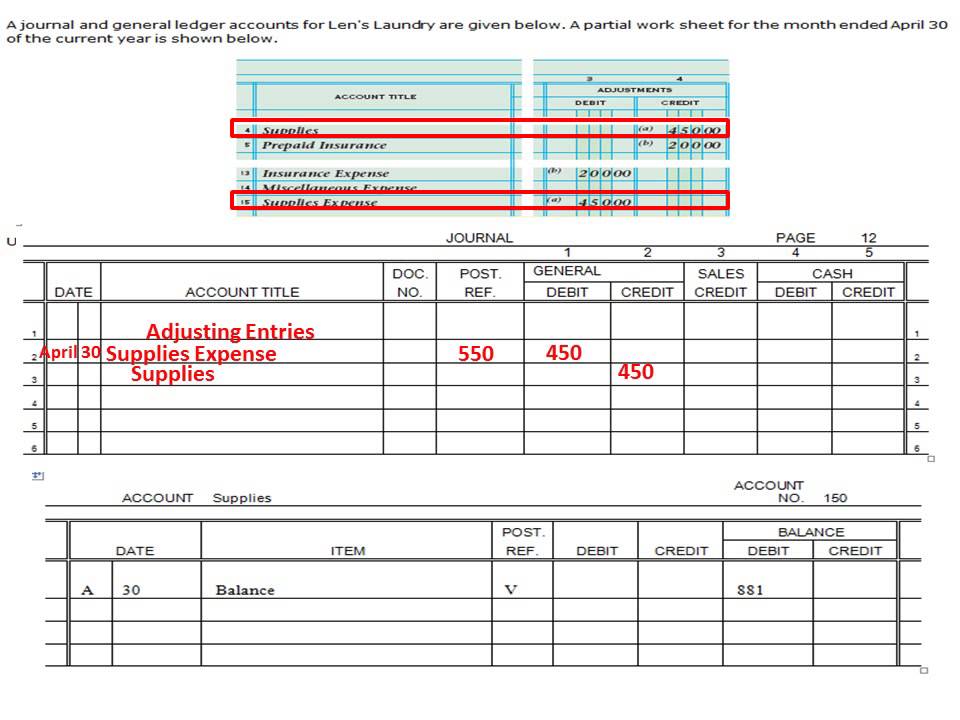

- In this chapter, you will learn the different types of adjusting entries and how to prepare them.

- For example, if you place an online order in September and that item does not arrive until October, the company you ordered from would record the cost of that item as unearned revenue.

- The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement.

Your Revenue Reporting May Be Inaccurate

One frequent mistake in adjusting entries is the failure to recognize accrued expenses. Businesses often overlook expenses that have been incurred but not yet paid, such as utilities or wages. This oversight can lead to an understatement of liabilities and expenses, distorting the financial statements. For instance, if a company forgets to record accrued wages at the end of the period, the expense will be understated, and net income will appear higher than it actually is.

Comprehensive Guide to Inventory Accounting

The same adjusting entry above will be made at the end of the month for 12 months to bring the Prepaid Rent amount down by $1,000 each month. Here is an example of the Prepaid Rent account balance at the end of October. The same adjusting entry above will be made at the end of the month for 12 months to bring the Prepaid Insurance amount down by $100 each month.

To record accrued revenue, an adjusting entry is made to increase the revenue account and increase the corresponding asset account. Adjusting entries significantly influence the accuracy and reliability of financial statements, ensuring that they present a true and fair view of a company’s financial position. Adjusting entries are a crucial part of the accounting process and are usually made on the last day of an accounting period. They are made so that financial statements reflect the revenues earned and expenses incurred during the accounting period.

Similarly, under the realization concept, all expenses incurred during the current year are recognized as expenses of the current year, irrespective of whether cash has been paid or not. Also, according to the realization concept, all revenues earned during the current year are recognized as revenue for the current year, regardless of whether cash has been received or not. An adjustment involves making a correct record of a transaction that has not been recorded or that has been entered in an incomplete or wrong way.

In such cases, therefore an overdraft would be created in his books of accounts and he will have to adjust it when he receives the balance by making an adjusting entry. Therefore, the entries made that at the end of the accounting year to update and correct the accounting records are called adjusting entries. Therefore, it is necessary to find out the transactions relating to the current accounting period that have not been recorded so far or which have been entered but incompletely or incorrectly. When you depreciate an asset, you make a single payment for it, but disperse the expense over multiple accounting periods.

The primary distinction between cash and accrual accounting is in the timing of when expenses and revenues are recognized. With cash accounting, this occurs only when money is received for goods or services. Accrual accounting instead allows for a lag between payment and product (e.g., with purchases made on credit). Adjusting journal entries are used to reconcile transactions that have not yet closed, but that straddle accounting periods. These can be either payments or expenses whereby the payment does not occur at the same time as delivery.