The accounting equation is balanced, asshown on the balance sheet, because total assets equal $29,965 asdo the total liabilities and stockholders’ equity. Remember that the balance sheet represents theaccounting equation, where assets equal liabilities plusstockholders’ equity. Once all of the adjusting entries have been posted to thegeneral ledger, we are ready to start working on preparing theadjusted trial balance. Preparing an adjusted trial balance is thesixth step in the accounting cycle. An adjusted trialbalance is a list of all accounts in the general ledger,including adjusting entries, which have nonzero balances. Thistrial balance is an important step in the accounting processbecause it helps identify any computational errors throughout thefirst five steps in the cycle.

How to cut the cost on your financial transactions

The statement of retained earnings always leads with beginning retained earnings. Beginning retained earnings carry over from the previous period’s ending retained earnings balance. Since this is the first month of business for Printing Plus, there is no beginning retained earnings 9 ways your firm can find new clients balance. Notice the net income of $4,665 from the income statement is carried over to the statement of retained earnings. Dividends are taken away from the sum of beginning retained earnings and net income to get the ending retained earnings balance of $4,565 for January.

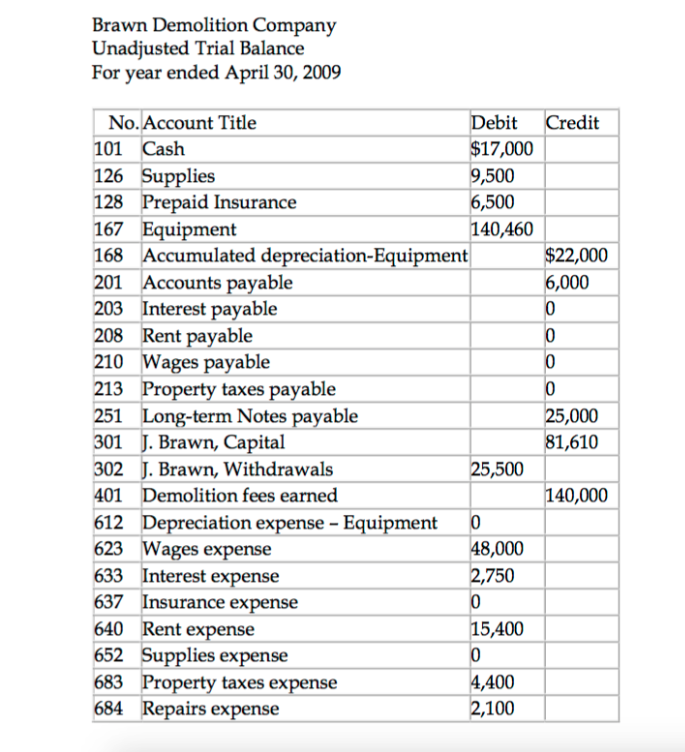

Unadjusted Trial Balance

The statement of retained earnings will include beginning retained earnings, any net income (loss) (found on the income statement), and dividends. The balance sheet is going to include assets, contra assets, liabilities, and stockholder equity accounts, including ending retained earnings and common stock. To prepare the financial statements, a company will look at theadjusted trial balance for account information.

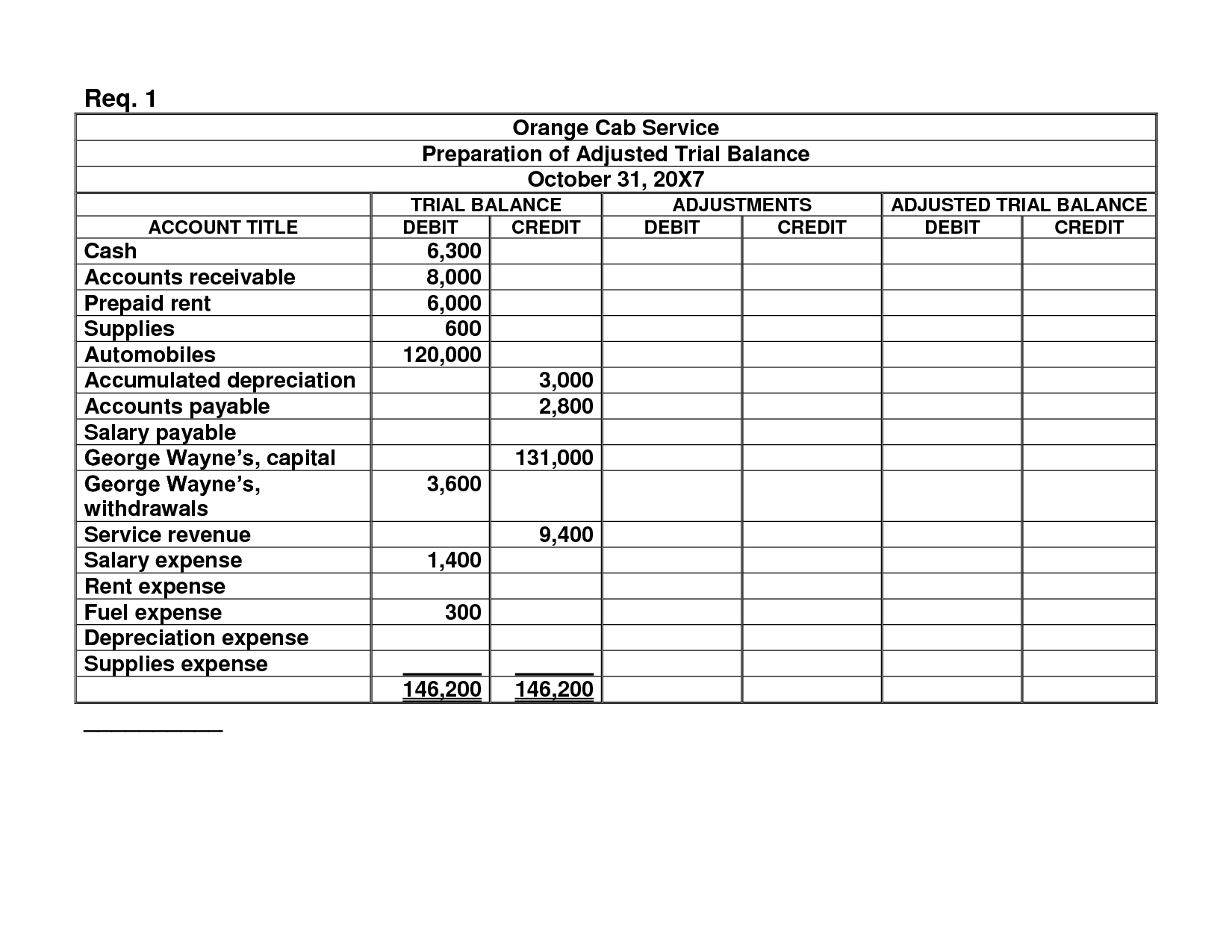

Adjustments from unadjusted trial balance

For example,IFRS-based financial statements are only required to report thecurrent period of information and the information for the priorperiod. Looking at the asset section of the balance sheet, AccumulatedDepreciation–Equipment is included as a contra asset account toequipment. The accumulated depreciation ($75) is taken away fromthe original cost of the equipment ($3,500) to show the book valueof equipment ($3,425).

- Once all accounts have balances in the adjusted trial balance columns, add the debits and credits to make sure they are equal.

- Dividends are taken away from the sum ofbeginning retained earnings and net income to get the endingretained earnings balance of $4,565 for January.

- The unadjusted trial balance is the initial report you use to check for errors, and the adjusted trial balance includes adjustments for errors.

- This gross misreporting misledinvestors and led to the removal of CeladonGroup from the New York Stock Exchange.

- After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

Income Statement

The biggest goal of a trial balance is to find accounting errors and transposition errors like switching digits. By highlighting these mistakes, the trial balance acts as an accuracy check for a business, mitigating the risk of inaccuracies before you generate final financial statements. Any difference indicates that there is accounting error in the journal entries or in the ledger or in the calculations.

Just like in the unadjusted trial balance, total debits and total credits should be equal. To exemplify the procedure of preparing an adjusted trial balance, we shall take an unadjusted trial balance and convert the same into an adjusted trial balance by incorporating some adjusting entries into it. To simplify the procedure, we shall use the second method in our example. You could also take the unadjusted trial balance and simply add the adjustments to the accounts that have been changed. In many ways this is faster for smaller companies because very few accounts will need to be altered. By providing a snapshot of all ledger accounts within a given accounting period, the trial balance helps business owners and accounting teams in reviewing accuracy.

This method is usually used by small companies where only a few adjusting entries are found at the end of the accounting period. In this method, the adjusting entries are directly incorporated into the unadjusted trial balance to convert it to an adjusted trial balance. An adjusted trial balance is a listing of all company accounts that will appear on the financial statements after year-end adjusting journal entries have been made. While an unadjusted trial balance may uncover mathematical errors, the following types help in eliminating accounting errors and ensuring accurate financial statements.

An adjusted trial balance is prepared after adjusting entries are made and posted to the ledger. In this lesson, we will discuss what an adjusted trial balance is and illustrate how it works. Now that the trial balance is made, it can be posted to the accounting worksheet and the financial statements can be prepared. Once all the accounts are posted, you have to check to see whether it is in balance. Preparing an adjusted trial balance is the fifth step in the accounting cycle and is the last step before financial statements can be produced. A trial balance plays a major role in the accounting cycle, notably at the end of an accounting period before generating financial statements.

From thisinformation, the company will begin constructing each of thestatements, beginning with the income statement. The statement ofretained earnings will include beginning retained earnings, any netincome (loss) (found on the income statement), and dividends. Thebalance sheet is going to include assets, contra assets,liabilities, and stockholder equity accounts, including endingretained earnings and common stock. There are five sets of columns, each set having a column for debit and credit, for a total of 10 columns. The five column sets are the trial balance, adjustments, adjusted trial balance, income statement, and the balance sheet. After a company posts its day-to-day journal entries, it can begin transferring that information to the trial balance columns of the 10-column worksheet.

This gross misreporting misled investors and led to the removal of Celadon Group from the New York Stock Exchange. Not only did this negatively impact Celadon Group’s stock price and lead to criminal investigations, but investors and lenders were left to wonder what might happen to their investment. After incorporating the adjustments above, the adjusted trial balance would look like this. In Completing the Accounting Cycle, we continue our discussionof the accounting cycle, completing the last steps of journalizingand posting closing entries and preparing a post-closing trialbalance. The salon had previouslyused cash basis accounting to prepare its financial records but nowconsiders switching to an accrual basis method.