Accrued expenses are expenses made but that the business hasn’t paid for yet, such as salaries or interest expense. There’s an accounting principle you have to comply with known as the matching principle. The matching principle says that revenue is recognized when earned and expenses when they occur (not when they’re paid). Adjusting entries are usually made at the end of an accounting period. They can, however, be made at the end of a quarter, a month, or even at the end of a day, depending on the accounting procedures and the nature of business carried on by the company. Accumulated Depreciation appears in the asset section of the balance sheet, so it is not closed out at the end of the month.

Unearned Revenues

This could be due to an error in the original journal entry, the need to accrue expenses or revenue, or the need to record depreciation. Amortization is the allocation of the cost of an intangible asset over its useful life. To record amortization, an accountant would debit an expense account and credit an accumulated amortization account.

Business License Tax – Deferred Expense

- Accrued expenses and accrued revenues – Many times companies will incur expenses but won’t have to pay for them until the next month.

- Here are descriptions of each type, plus example scenarios and how to make the entries.

- The revenue recognition principle requires businesses to recognize revenue when it is earned, regardless of when payment is received.

- Without adjusting entries to the journal, there would remain unresolved transactions that are yet to close.

- These entries are made at the end of an accounting period to adjust the accounts to their correct balances.

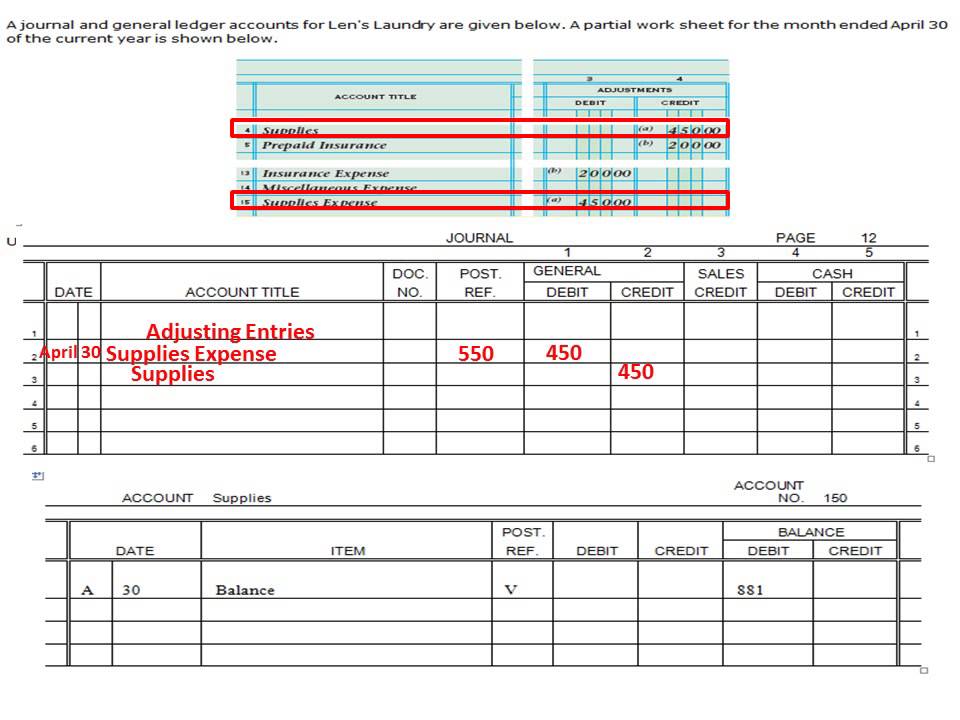

Deferrals involve postponing the recognition of revenues and expenses to future periods. This type of adjusting entry is used when cash has been received or paid, but the related revenue or expense has not yet been earned or incurred. For example, if a company receives payment in advance for a service to be provided over several months, the initial cash receipt is recorded as a liability (unearned revenue). As the service is performed, the liability is gradually reduced, and revenue is recognized. Similarly, prepaid expenses, such as insurance or rent, are initially recorded as assets. Over time, as the benefit of these prepaid expenses is realized, the asset is reduced, and the expense is recognized.

Common Examples of Adjustment Entries

For instance, an accrued expense may be rent that is paid at the end of the month, even though a firm is able to occupy the space at the beginning of the month that has not yet been paid. Uncollected revenue is revenue that is earned during a period but not collected during that period. Such revenues are recorded by making an adjusting entry at the end of the accounting period. Deferrals are adjusting entries for items purchased in advance and used up in the future (deferred expenses) or when cash is received in advance and earned in the future (deferred revenue).

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. In December, you record it as prepaid rent expense, debited from an expense account. Then, come January, you want to record your rent expense for the month. You’ll move January’s portion of the prepaid rent from an asset to an expense. In the accounting cycle, adjusting entries are made prior to preparing a trial balance and generating financial statements.

The Process of Recording Adjustment Entries

Assets depreciate by some amount every month as soon as it is purchased. This is reflected in an adjusting entry as a debit to the depreciation expense and payroll software equipment and credit accumulated depreciation by the same amount. If you don’t make adjusting entries, your income and expenses won’t match up correctly.

This transaction is recorded as a prepayment until the expenses are incurred. Only expenses that are incurred are recorded, the rest are booked as prepaid expenses. The purpose of adjusting entries is to assign an appropriate portion of revenue and expenses to the appropriate accounting period. By making adjusting entries, a portion of revenue is assigned to the accounting period in which it is earned, and a portion of expenses is assigned to the accounting period in which it is incurred.

No matter what type of accounting you use, if you have a bookkeeper, they’ll handle any and all adjusting entries for you. If you do your own accounting, and you use the accrual system of accounting, you’ll need to make your own adjusting entries. To make an adjusting entry, you don’t literally go back and change a journal entry—there’s no eraser or delete key involved. More specifically, deferred revenue is revenue that a customer pays the business, for services that haven’t been received yet, such as yearly memberships and subscriptions. If you haven’t decided whether to use cash or accrual basis as the timing of documentation for your small business accounting, our guide on the basis of accounting can help you decide. For example, let’s assume that in December you bill a client for $1000 worth of service.

To avoid this mistake, it is important to record transactions as soon as possible and ensure that they are accurate. Adjustment entries can impact a business’s cash flow by affecting the timing of cash inflows and outflows. For example, if an adjustment entry is made to increase accounts receivable, this will increase the amount of cash that the business expects to receive in the future. On the other hand, if an adjustment entry is made to increase accounts payable, this will decrease the amount of cash that the business expects to pay in the future. Accounting software can be used to simplify the process of recording adjustment entries. Most accounting software has built-in features that allow for the easy creation and recording of adjustment entries.

The same process applies to recording accounts payable and business expenses. When cash is received it’s recorded as a liability since it hasn’t been earned yet by the business. Over time, this liability is turned into revenue until it’s fully earned.

The process of recording adjustment entries can be complex, but it is essential for maintaining the integrity of financial statements. For example, if you place an online order in September and that item does not arrive until October, the company you ordered from would record the cost of that item as unearned revenue. The company would make adjusting entry for September (the month you ordered) debiting unearned revenue and crediting revenue. A company receiving the cash for benefits yet to be delivered will have to record the amount in an unearned revenue liability account. Then, an adjusting entry to recognize the revenue is used as necessary.